One of the things that break my heart is seeing others needlessly suffer.

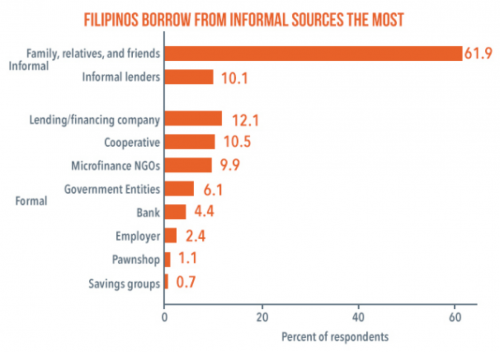

According to the Bangko Sentral ng Pilipinas (BSP), as of 2015, around 47% of all adult Filipinos had an outstanding loan. The average interest rate of a bank is about 1.4%, yet 72% of individuals who had loans borrowed from informal lenders like family and friends, or worse, from loan sharks who charge interest rates as high as 20%.

This means that majority of Filipinos borrowers suffer from usurious interest rates. The world may be in the age of blockchain and cryptocurrency, but in places like the Philippines, the poor are still suffering from Shylock-style lending.

Figure 1. Source: 2015 National Baseline Survey on Financial Inclusion (BSP)

Yet as costly and inconvenient as this may sound, as foolish as it is, people continue to apply for and accept these loans for various reasons, including ineligibility to borrow from formal lenders, ignorance, and lack of access to better options. For example, the credit card penetration in the Philippines is said to be at 5% of the population. Where do the other 95% draw credit from? Their options are between no credit or expensive credit.

We had to change that. We asked ourselves, “Why do those who earn the least continue to pay the most for goods and services? Why do those who need the most have the least access?”

So we quietly created a loans platform for workers, people who are gainfully employed, who need an affordable, fast, and easily-accessible personal loan.

We didn’t simply want to become a “digital loan shark” like what other lending companies were doing. While most lending companies were trying to improve the operation of the lender by adding tech to the lending process, we wanted to improve the life of the borrower. And the only way to do that was to aim for a drastically lower interest. If loan sharks were at 10-20% a month, and digital lenders were at 5-10%, we aimed for a 1-2% interest, and we were going to make it our goal to find ways to continue to lower this rate.

We called our platform Bridge Access

After a one year Proof of Concept (POC) and a few months of going live, we have gleaned valuable insights, such as:

- The average loan value per person was double than we projected.

- The repayment rate was 10% higher than what we expected.

- Savings from refinancing can be used to provide savings, insurance, and investments, turning a liability into a source of security.

There were other technological and financial learnings but the best has to be learning about the impact we were having on the lives of our customers. We knew that offering a very low-interest rate would improve their financial situation, but we didn’t know just how life-changing this would be. From fathers being able to take their families to the movies, to employees being able to buy property, to daughters being able to pay for a parent’s chemotherapy, our office was filled with story after story of how our low-cost loans fundamentally improved their lives. We’ll be sharing more of these stories with you as we compile them. It’s amazing what good we can do when we give an individual Access.

We continue to improve the Bridge Access platform, adding more lending options, investment and insurance products, and payment options for e-commerce. This includes a layaway program allowing people, who previously could not shop online, to purchase items in installments, truly making a better life more accessible. From online shopping to health services, from financial products to travel, the options of even the lowest-ranked worker are better than ever with Bridge Access.

Some of our partners

Here’s the best part: It’s totally free to become a member of Bridge Access. We have partnered our technology with some of the most dynamic companies, including banks, lenders, employers, e-wallets, e-money, and merchants, to make work life more rewarding. By reducing the cost and risk of serving low-cost markets, we’re able to pass on the savings for more options and at better prices too.

Did I mention we also have a points system? Every transaction on Bridge Access is a chance to win in one of our raffles. We want to incentivize smarter financial decisions, and what better way than to improve access, reduce prices, and add rewards?

We Dream of Access

In our part of the world, seeing a beggar on the street, driving past a naked baby running out of a shanty, or hearing stories of families suffering from generational debt, are too common. It’s easy to become desensitized, to simply turn a blind eye, and to busy oneself with our own concerns. I’m happy that our team has joined the ranks of those who choose to do something to improve the lives of others. And I’m excited for what technology combined with compassion can do for all of us because improving our neighbor benefits us as well. I am most excited for even more stories of lives significantly made better from having Access.

To learn more about Bridge Access, visit bridgeaccess.life